The landscape of European digital commerce is undergoing a fundamental shift. While Western European markets have long been viewed as the mature, saturated engines of the continent’s online economy, the next five years will tell a different story. According to a comprehensive new report from the Germany-based ecommerce intelligence firm ECDB, the epicenter of growth is migrating eastward and southward. Between 2025 and 2029, the fastest-growing digital marketplaces in Europe will be dominated by emerging economies, with Turkey and Bulgaria leading a transformative charge.

Main Facts: The New Rankings of Growth

The ECDB study, which analyzed projected compound annual growth rates (CAGR) for online retail across the continent, paints a clear picture of a market in transition. The data suggests that as traditional hubs like the UK, France, and Germany approach maturity, capital and consumer interest are pivoting toward regions where digital infrastructure is currently scaling at an unprecedented pace.

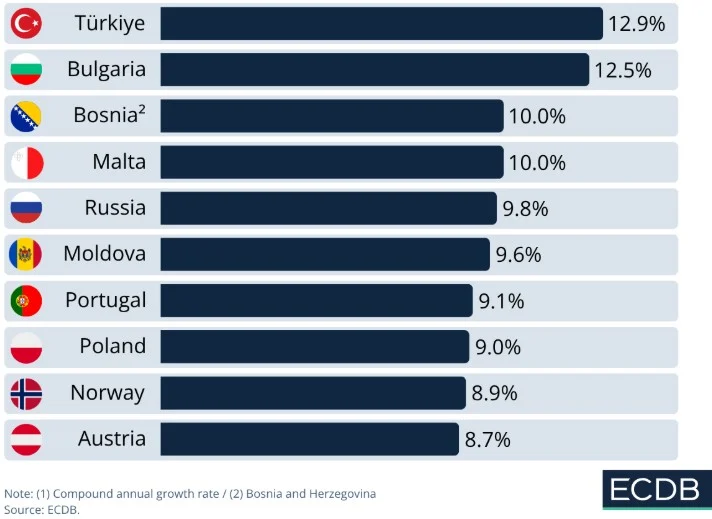

Turkey sits at the summit of this ranking, with a projected average annual growth rate of 12.9% through 2029. It is followed closely by Bulgaria, which is expected to see its ecommerce sector expand by 12.5% annually. The third position is shared by Bosnia and Herzegovina and Malta, both projecting a robust 10.0% growth rate.

This shift is not merely statistical; it represents a convergence of rising internet penetration, evolving payment systems, and a burgeoning middle class that is increasingly comfortable with digital-first retail environments.

Chronology of the Shift: How We Arrived Here

To understand the current trajectory, one must look at the timeline of European digital maturation:

- 2015–2020: The Foundation Phase. During this period, Northern and Western Europe solidified their dominance. Infrastructure was built, and consumer trust in digital payments reached a critical mass.

- 2020–2023: The Pandemic Catalyst. COVID-19 acted as a forced accelerator. Even in countries with lower digital adoption, the necessity of remote shopping forced retailers to pivot and consumers to adapt.

- 2023–2024: The Infrastructure Pivot. As traditional markets reached a plateau of saturation, major logistics players and marketplace giants (such as Zalando) began shifting their strategic focus toward Southeastern Europe.

- 2025–2029: The Expansion Era. The current forecast period reflects the transition from "adoption" to "integration." Countries that were once considered peripheral are now the primary targets for international investment, as the digital ecosystem moves from infancy to maturity.

Supporting Data: By the Numbers

The scale of this growth varies significantly by market size and existing economic conditions.

Turkey remains the titan of this list. With a population of approximately 86 million, the sheer scale of the Turkish market is unmatched by its peers in the top ten. Recent government figures indicate that Turkish online spending reached 86 billion euros last year—a 16% increase. This serves as a testament to the fact that even in a relatively large, developed market, the "digital catch-up" is far from over.

In contrast, Bulgaria represents the "nascent market" archetype. Despite its smaller size—recording approximately 1.2 billion euros in online spending last year—the growth potential is fueled by low baseline adoption. As major players like Zalando prepare to enter the market, the infrastructure is expected to modernize rapidly, acting as a catalyst for consumer behavior shifts.

Russia, despite geopolitical and macroeconomic complexities, remains a significant force. Home to industry giants Ozon and Wildberries, the country ranks fifth on the list with a projected annual growth of 9.8%. Meanwhile, Poland’s appearance in the eighth spot highlights that even Central European nations, which have already seen significant growth, still possess the structural capacity for further expansion.

Official Perspectives: Why the Shift is Structural

ECDB analysts are clear that this movement is not a fluke of short-term volatility but rather a calculated, structural evolution. "The reasons for their fast development are structural and by no means accidental," the firm noted in its latest release.

For industry observers, the primary drivers are threefold:

- Late-Mover Advantage: Unlike Western European countries, which had to retrofit their retail sectors to accommodate digital commerce, emerging economies are leapfrogging older technologies, implementing mobile-first payment solutions and sophisticated logistics networks from the outset.

- Marketplace Ecosystems: The entry of global and regional marketplaces—such as the recent expansion strategies of Zalando or the continued dominance of local giants like Wildberries—has provided the necessary scale to entice hesitant consumers.

- Digital Literacy and Demographics: In many of these nations, the demographic profile is younger and more tech-savvy than in the aging populations of Western Europe, creating a natural affinity for digital retail.

Implications for Investors and Retailers

The implications for the broader retail sector are profound. For international retailers, the strategy of "Western-first" is becoming increasingly obsolete. The data suggests that the highest return on investment (ROI) in the coming half-decade will likely be found in markets that are currently "under-indexed" in terms of digital penetration.

The Logistics Challenge

As these markets grow, the pressure on logistics providers will be immense. The "last mile" delivery in countries like Bosnia and Herzegovina or Bulgaria requires a different logistical approach than in the dense urban centers of Germany. Investors are already pivoting, focusing on firms that specialize in cross-border logistics and automated warehousing designed for smaller, fragmented markets.

The Role of Payment Innovation

The growth in these regions is inextricably linked to the democratization of payments. In Turkey and across the Balkans, the shift from cash-on-delivery to digital wallets and "Buy Now, Pay Later" (BNPL) schemes has been a primary driver of trust. Retailers entering these markets must prioritize local payment integration, or risk losing the consumer base entirely.

Regulatory Landscapes

As these ecommerce markets mature, the regulatory environment is also expected to tighten. We are already seeing a push for harmonized digital consumer protection laws across the EU, which will impact markets like Bulgaria and Malta. Companies that act now to ensure compliance will find themselves at a significant advantage as the regulatory landscape catches up to the volume of trade.

Conclusion: A New Center of Gravity

The ECDB report provides a clear roadmap for the future of European commerce. The "growth race" is being won by those who are currently building the digital infrastructure of tomorrow.

While the established giants of Western Europe will remain vital, the engines of innovation and the highest percentage growth rates will continue to emanate from the East and South. For the retail sector, the takeaway is simple: the map of European ecommerce is being redrawn. Success in the next five years will depend not on dominating mature, saturated markets, but on participating in the rapid, structural ascent of emerging digital economies.

As we look toward 2029, the dominance of Turkey, Bulgaria, and their neighbors in this growth ranking serves as a powerful reminder that in the digital age, geography is no longer a constraint—it is a launchpad for unprecedented economic opportunity. The race is on, and the frontrunners are already making their move.