The landscape of European digital commerce is undergoing a profound structural shift. While Western European giants have long defined the continent’s online shopping habits, the next five years will be defined by the rapid ascent of emerging markets in the East and Southeast. According to a comprehensive new analysis by Germany-based ecommerce intelligence firm ECDB, Turkey and Bulgaria are poised to lead the continent in growth, outperforming more mature economies by a significant margin.

As the industry looks toward 2029, the data paints a clear picture: the "growth race" is no longer happening in London, Paris, or Berlin, but in markets where infrastructure development and digital adoption are converging to create a perfect storm of economic opportunity.

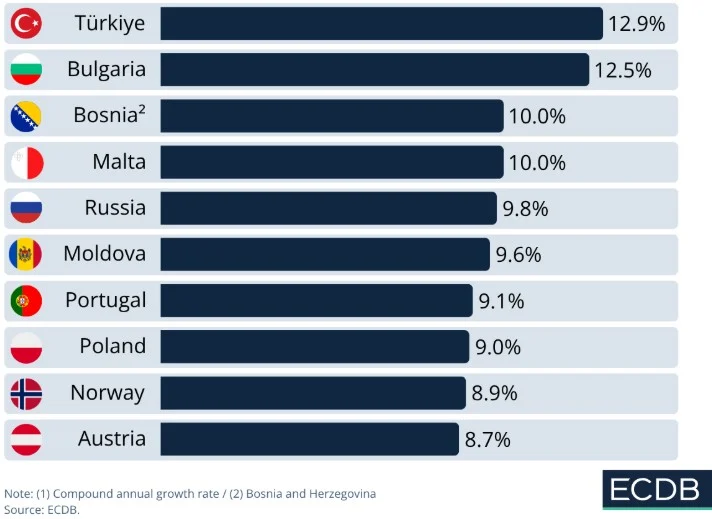

Main Facts: The New Champions of Ecommerce

The ECDB report, which analyzes average annual growth rates between 2025 and 2029, highlights a distinct geographical trend. Turkey takes the top spot with a projected annual growth rate of 12.9%. Following closely is Bulgaria, with a forecast of 12.5%.

The findings underscore that the most significant expansion is occurring in nations that are transitioning from nascent online retail environments to fully digitized marketplaces. While these countries may currently represent a smaller portion of the total European online spend compared to established giants like Germany or the UK, their trajectory suggests a rapid narrowing of that gap.

The Top Growth Contenders

- Turkey: 12.9% (Projected Annual Growth)

- Bulgaria: 12.5%

- Bosnia and Herzegovina: 10.0%

- Malta: 10.0%

- Russia: 9.8%

This data suggests that investors, logistics providers, and cross-border retailers should pivot their focus toward these regions. The inclusion of Russia in the top five—despite complex geopolitical headwinds—serves as a reminder that the scale of players like Ozon and Wildberries continues to influence regional averages, even as other, smaller economies gain momentum through structural integration.

Chronology: The Evolution of European Digital Retail

To understand why these specific nations are leading the charge, one must look at the timeline of digital transformation in the region.

Phase 1: The Foundation (2015–2020)

During the latter half of the 2010s, European ecommerce was characterized by the dominance of Western platforms. Eastern and Southeastern European markets were largely characterized by cash-on-delivery systems and underdeveloped logistics networks. Internet penetration was rising, but trust in digital payments remained a hurdle.

Phase 2: The Acceleration (2020–2024)

The global pandemic served as an exogenous shock that forced a decade’s worth of digital adoption into just two years. Turkey, in particular, leveraged its massive population of 86 million to create a domestic ecommerce ecosystem that reached approximately 86 billion euros in spending by 2024. In Bulgaria, meanwhile, the market began preparing for the arrival of major international players like Zalando, signaling that the region was finally "ready" for large-scale logistics investments.

Phase 3: The Scaling Era (2025–2029)

We are currently entering the third phase. The ECDB forecast covers this period, which is defined by the professionalization of the "last mile," the consolidation of marketplaces, and the normalization of digital payments. The growth is no longer speculative; it is rooted in the expansion of consumer choice and the maturation of national delivery infrastructures.

Supporting Data: By the Numbers

The disparity between market size and growth potential is one of the most compelling aspects of the ECDB study. Turkey stands as an outlier in the top rankings; its 86-million-strong population provides a massive, scalable consumer base that is far larger than those of the other top-tier growth nations.

In contrast, Bulgaria represents a "low-base" success story. With online spending totaling roughly 1.2 billion euros last year, the country is starting from a position where even modest infrastructure improvements result in double-digit percentage gains.

Comparative Regional Analysis

The report identifies that the drivers of growth are not uniform. In Poland, which holds the eighth spot, growth is characterized by "steady expansion"—a result of a well-established, stable, and highly competitive domestic market. Conversely, in the Balkan region, growth is driven by the "catching up" effect. As these countries integrate more deeply with the European single market, the regulatory barriers to cross-border trade are lowering, making it easier for local merchants to sell internationally and for global brands to enter these markets.

Official Perspectives and Expert Analysis

ECDB’s analysts emphasize that this shift is "by no means accidental." The growth is structural, driven by a combination of deliberate government investment in digital infrastructure and the organic maturation of the private sector.

"The reasons for their fast development are structural," the ECDB report notes. In many of these emerging markets, ecommerce was essentially in its infancy as recently as 2023. As consumers in these regions move from traditional retail to digital platforms, they are leapfrogging legacy systems—much like the mobile banking revolution that transformed emerging markets in Africa and Asia.

Market experts also point to the "marketplace effect." When a major platform enters a region—such as Zalando’s expansion into Bulgaria—it acts as a catalyst. It forces local competitors to upgrade their websites, improves local payment gateways, and creates a "halo effect" that benefits the entire logistics chain.

Implications for the Future of European Ecommerce

The findings from this report carry significant implications for stakeholders across the continent.

1. For Retailers and Brands

The "Western-first" strategy may soon be outdated. Brands that have yet to localize their offerings for the Turkish or Bulgarian markets are missing out on the fastest-growing customer segments in Europe. The key, however, is adaptation. These markets are not monolithic; they require distinct strategies regarding payment methods (e.g., the prevalence of specific digital wallets or local credit schemes) and logistics partnerships.

2. For Logistics and Infrastructure

The demand for "last-mile" delivery solutions in Southeastern Europe will skyrocket through 2029. We can expect an increase in the construction of fulfillment centers and a rise in the demand for automated sorting and delivery drones in dense urban centers like Istanbul or Sofia.

3. For Economic Policy

For the governments of these top-ten nations, the data serves as a mandate to continue investing in digital education and cybersecurity. If these nations can maintain a stable regulatory environment, they are likely to attract significant foreign direct investment (FDI) from global ecommerce giants looking to diversify their presence away from the saturated markets of Western Europe.

4. The "Catch-Up" Dynamic

As these markets grow, we can expect a gradual equalization of the "ecommerce experience" across Europe. By 2029, the gap between a consumer in Sofia and a consumer in Berlin regarding delivery speeds, return policies, and platform accessibility will likely be significantly smaller than it is today.

Conclusion: A Continent in Transition

The ECDB report is a clear signal that the center of gravity for European ecommerce is shifting. While Germany, France, and the UK will remain the largest markets by sheer volume for the foreseeable future, the dynamic growth is undeniably moving eastward and southward.

The next five years will be a test of resilience and adaptation. Countries like Turkey, Bulgaria, and the nations of the Balkans are no longer just "emerging"—they are becoming the primary drivers of the European digital economy. For businesses and policymakers alike, the lesson is clear: the future of European commerce is being written in the markets that are, today, innovating at the fastest pace. As we approach 2029, those who recognize this shift early will be the ones to define the next generation of the European digital retail landscape.