The current military conflict involving Iran has sent shockwaves through the global economy, acting as a catalyst for a sharp, uncomfortable spike in energy costs. For the average American consumer, this is not merely a macroeconomic abstraction; it is a reality felt at the pump and in the heating bill. According to a Pew Research Center survey conducted in late March 2026, 69% of U.S. adults identified themselves as extremely or very concerned about rising fuel prices stemming from the geopolitical instability in the Middle East.

As the conflict persists, the vulnerability of the global oil market has come into stark focus. To understand the current trajectory, it is necessary to examine the foundational dynamics of U.S. oil production, consumption, and the strategic decisions governing our national reserves.

The Global Powerhouse: U.S. Crude Production Trends

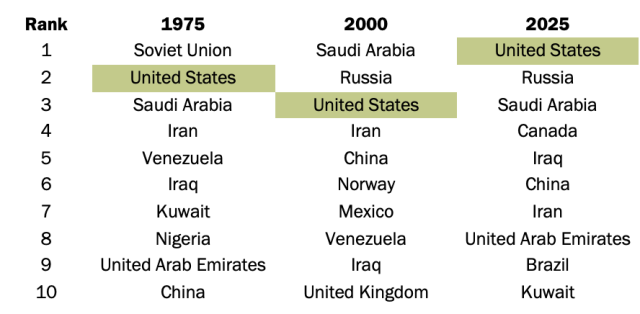

The United States has firmly cemented its position as the world’s leading producer of crude oil. While the U.S. has historically been a significant player—frequently ranking alongside industry titans like Russia and Saudi Arabia—the landscape shifted dramatically in 2018. That year, the U.S. secured the top spot globally, a position it has maintained through aggressive innovation and infrastructure development.

This ascent is primarily attributed to the widespread adoption of hydraulic fracturing, commonly known as "fracking." By unlocking vast reserves of oil and natural gas trapped in shale rock formations, the U.S. transformed its energy profile. Throughout the 2000s and into the 2010s, massive investments in fracking infrastructure allowed the U.S. to scale production to levels previously thought unattainable. Today, the U.S. not only leads in crude oil but also dominates the production of petroleum products—including gasoline, diesel, and jet fuel—as well as essential petrochemical feedstocks used in manufacturing plastics and synthetics.

Defining Terms: Oil, Gas, and Petroleum

The complexity of the energy market often leads to confusion regarding terminology. While often used interchangeably in casual conversation, these terms refer to distinct entities. Petroleum is an umbrella term covering both crude oil (the raw, unrefined hydrocarbon) and the refined products derived from it, such as gasoline and propane. Natural gas, conversely, is not classified as petroleum by major agencies like the U.S. Energy Information Administration (EIA) because it exists as a gas rather than a liquid. However, natural gas liquids (NGLs) are categorized as petroleum because they can be extracted as liquids during the processing of natural gas.

A Chronology of Supply and Consumption

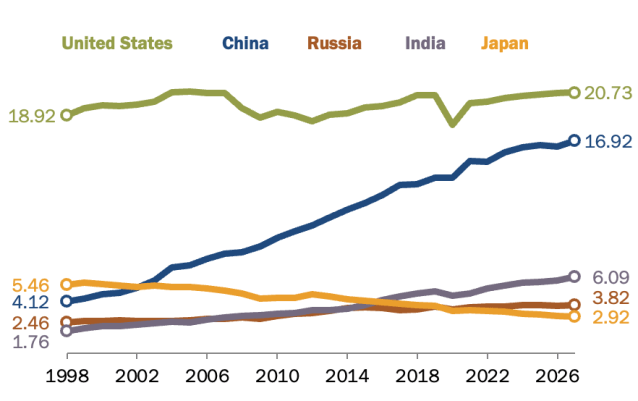

The U.S. energy story is not solely one of production; it is also one of immense demand. Since 1998, the United States has consistently accounted for roughly 20% of the world’s total oil consumption. While domestic production has reached historic highs, American appetite for liquid fuels remains the primary engine of global market activity.

The Rise of Chinese Demand

For decades, the U.S. stood unrivaled as the world’s primary consumer. However, the emergence of China as a manufacturing and industrial juggernaut has altered the calculus. Since 1998, Chinese oil consumption has quadrupled, rising from approximately 4 million barrels per day to roughly 17 million. China now accounts for about 16% of global consumption.

Analysts suggest that Chinese oil demand is approaching a turning point, with a peak expected as early as 2027. This shift is driven by a massive transition toward electrification; in 2025 alone, over 50% of all new vehicle sales in China were either electric or hybrid models. Furthermore, the country is diversifying its energy mix through high-speed rail expansion and the aggressive adoption of natural-gas-powered trucking fleets.

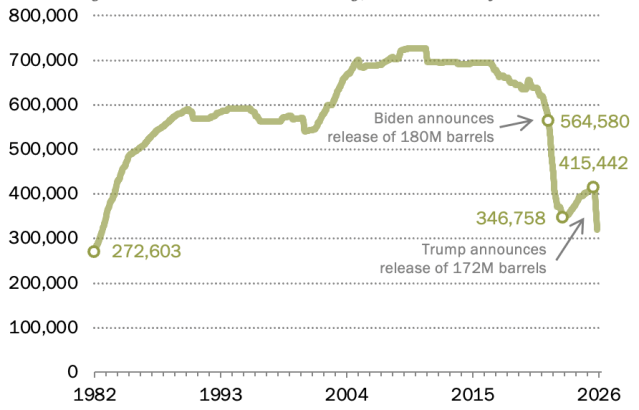

The Strategic Petroleum Reserve: A Buffer Under Pressure

One of the most visible markers of the current crisis is the state of the U.S. Strategic Petroleum Reserve (SPR). Established in 1975, the SPR acts as an emergency stockpile of crude oil, designed to mitigate the impact of major supply disruptions. Currently, the reserve sits at its lowest level since the early 1980s, a direct consequence of consecutive administrations attempting to dampen market volatility.

Recent Policy Interventions

- 2022 Surge: In response to price spikes, the Biden administration authorized the largest-ever release from the SPR, totaling 180 million barrels over seven months.

- 2026 Response: Following the outbreak of the Iran conflict, the current administration announced a second-largest withdrawal of 172 million barrels, intended to be executed over a four-month period.

These strategic drawdowns have reduced the SPR to roughly half of its capacity compared to five years ago. While these measures were designed to provide immediate relief to consumers, they have sparked intense debate among policymakers about the limits of emergency reserves and the necessity of long-term energy security. Globally, the International Energy Agency (IEA) has described the ongoing situation as the "largest supply disruption in history," prompting an unprecedented international release of emergency stocks.

Global Exposure: The Middle East Factor

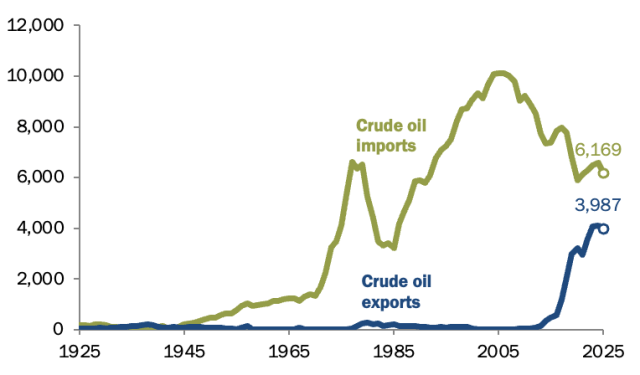

A common misconception is that the U.S. is heavily dependent on Middle Eastern oil. While the U.S. remains a net importer—bringing in roughly 2.2 million barrels per day in 2025—the sources of these imports have shifted significantly. The vast majority of U.S. imports (57%) currently originate from Canada, rather than the Middle East.

In 2024, only 3% of the oil consumed in the United States was sourced from the Middle East, a substantial decline from 8% in 2017. This indicates that the U.S. economy is far less "exposed" to disruptions in the Persian Gulf than other major global economies. For instance, Japan remains heavily reliant on the region, with nearly 80% of its domestic consumption sourced from Middle Eastern suppliers.

Why Does the U.S. Import at All?

If the U.S. is the world’s top producer, why does it remain a net importer? The answer lies in the composition of the oil. Much of the U.S. domestic output consists of "light" shale oil. Conversely, many domestic refineries are complex, multi-billion-dollar facilities specifically engineered to process "heavy" crude oil. Consequently, it is often more economically efficient for refineries to import heavy crude from abroad than to reconfigure their entire processing infrastructure to accommodate lighter domestic supplies.

Economic and Geopolitical Implications

The ongoing conflict in Iran has created a precarious environment for global markets. The "risk premium" attached to oil prices has increased as investors account for potential bottlenecks in transit points like the Strait of Hormuz.

Domestic Economic Impact

For the American consumer, the immediate impact is a rise in the cost of transportation and goods. Energy-intensive industries, including shipping, agriculture, and manufacturing, are passing these costs on to the end-user, contributing to broader inflationary pressures.

The Path Forward

The volatility has forced a reckoning regarding energy policy. Several nations, including the U.S., are looking toward a dual strategy: maximizing domestic production while accelerating the transition to alternative energy sources to insulate the economy from future shocks.

Governmental responses have been swift. Dozens of countries, including the U.S., have explored or implemented tax relief on fuel and other temporary fiscal measures to cushion the blow for low-to-middle-income households. However, the consensus among economists is that such measures are stop-gaps rather than solutions.

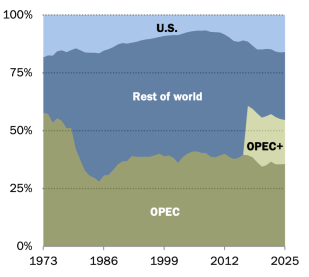

The current situation underscores a fundamental truth of the 21st-century energy market: although the United States has achieved a level of energy production that was unthinkable twenty years ago, it remains inextricably linked to a global network. The shift in production share—now 16% of the global crude market, the highest since the 1980s—provides a buffer, but it does not grant total immunity from the geopolitical realities of the Middle East.

As the Iran conflict continues, the interplay between domestic production, the integrity of the Strategic Petroleum Reserve, and the global reliance on Middle Eastern energy will remain the defining factors of the American economic narrative. For now, policymakers are tasked with the delicate balance of maintaining energy affordability while securing a transition that reduces long-term reliance on the volatile regions of the world.