For generations, the "American Dream" was anchored by the promise of homeownership—a milestone that signaled stability, maturity, and the accumulation of intergenerational wealth. However, for today’s young adults, that dream is increasingly morphing into a fiscal nightmare. Caught in a pincer movement of surging property values and stagnant wage growth, those under the age of 40 are facing a housing market more daunting than any seen in decades.

A comprehensive new study by the Pew Research Center confirms what many have felt anecdotally: the path to owning a home has become significantly more treacherous since 2019. With a stark rise in price-to-income ratios and an explosion in monthly carrying costs, the traditional gateway to the middle class is rapidly closing for millions of Americans.

The Shrinking Horizon: Main Facts

The core of the issue lies in a fundamental disconnect between the cost of shelter and the earning power of young workers. According to the data, the national median home price has soared, far outpacing the growth of household incomes for those under 40.

As of 2024, the price-to-income ratio—a critical metric used by economists to gauge affordability—stands at 3.5. To put this in perspective, this figure has not been this high since the mid-2000s, a period famously defined by the catastrophic housing bubble that triggered the Great Recession. Prior to the turn of the millennium, this ratio hovered steadily around 2.5, suggesting that the current market is historically anomalous and punishingly expensive.

The implications are immediate. In 2019, 56% of renter households headed by someone under 40 earned enough to feasibly afford the monthly costs of a home. By 2024, that number plummeted to 37%. This decline is not merely a reflection of sticker prices; it is a cumulative effect of higher mortgage interest rates, rising property taxes, and increasing insurance premiums.

A Chronology of Economic Drift

To understand the current crisis, one must look at the trajectory of the last half-century.

The Mid-1970s to 1990s: For decades, the price-to-income ratio remained relatively stable. In 1975, a household could expect a ratio of 2.5. This era allowed for a predictable accumulation of equity, where housing costs were tethered to the reality of labor market wages.

The Early 2000s Bubble: The first signs of structural instability appeared around 2003, as ratios began to climb above 3.0. By 2006, the peak of the pre-recession bubble, the ratio hit 3.6. The subsequent crash saw a temporary correction, but the market never truly returned to the historical baseline of 2.5.

The 2019-2024 Pivot: The most dramatic shift has occurred in the last five years. While the pandemic initially sparked uncertainty, the subsequent rebound in housing demand—coupled with supply constraints—sent prices into a vertical climb. By 2024, the median home price reached $350,000, while the income for those under 40 struggled to keep pace. Simultaneously, the average 30-year fixed mortgage rate surged from a comfortable 3.9% in 2019 to a punishing 6.7% in 2024, effectively doubling the interest burden for new buyers.

The Anatomy of the Crisis: Supporting Data

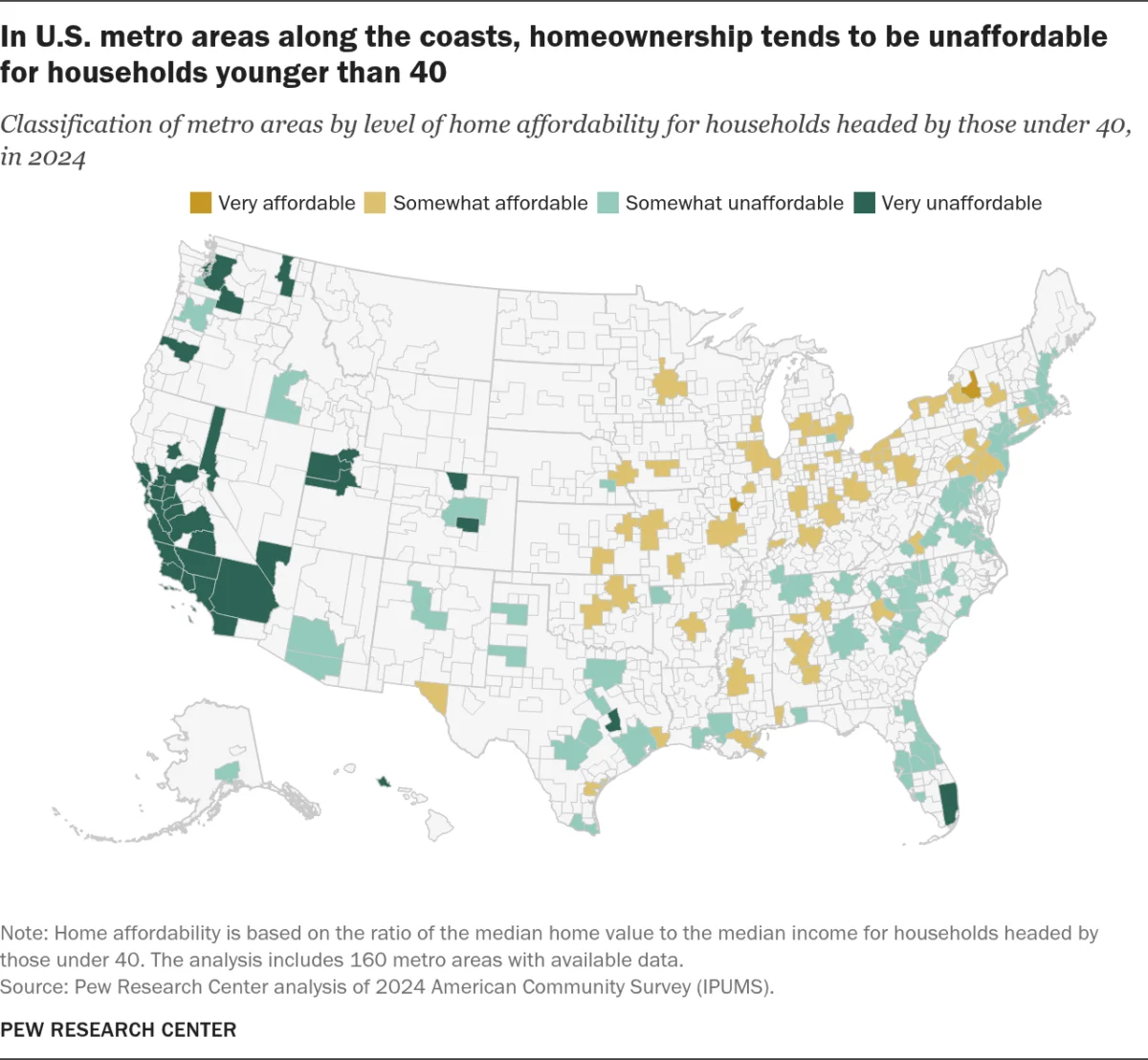

The data reveals a geographic divide that is as profound as the generational one. The Pew Research Center analyzed 160 metropolitan areas, finding that in 142 of them, home values grew faster than incomes between 2019 and 2024.

In 2019, 59% of these areas were classified as "very or somewhat affordable." By 2024, that trend had completely inverted, with 61% of those same areas now labeled as "somewhat or very unaffordable."

The Coastal Divide

The geography of the crisis is concentrated along the coasts. In states like California and Hawaii, the dream of homeownership has reached a point of near-impossibility for the average young household. California’s Santa Maria-Santa Barbara metro area, for instance, leads the nation in unaffordability with a staggering 9.6 price-to-income ratio. Similarly, Urban Honolulu, HI, and various Southern California hubs consistently show ratios exceeding 7.0.

Conversely, the most affordable regions are found in the industrial heartland and parts of the Northeast, such as Springfield, IL (2.3), Utica-Rome, NY (2.4), and Cleveland, OH (2.5). However, even in these areas, the trend lines are moving in the wrong direction, as the national housing shortage begins to bleed into more affordable markets.

The Barrier of Entry: The Down Payment Trap

While monthly mortgage payments are the most visible hurdle, the hidden killer of homeownership is the down payment. The Federal Reserve’s 2024 survey indicates that 70% of renters under age 40 identify the inability to afford a down payment as the primary reason they remain in the rental market.

As home prices rise, the savings required for a traditional 20% down payment have become insurmountable for those saddled with student loans, rising childcare costs, and the general inflationary pressures on basic goods. For many, the "nest egg" required to enter the market is a goal that recedes further with every year of saving.

Public Sentiment: A Generation Losing Faith

The psychological toll of this economic landscape is visible in the public’s outlook. A survey of 10,091 U.S. adults conducted in May 2026 reveals a deep-seated pessimism. Roughly 89% of adults under 40 believe it is harder to buy a home today than it was for their parents.

While 67% of Americans still consider buying a home a "good investment," the intensity of that belief is waning among the young. Only 24% of adults under 40 view it as a "very good" investment, compared to 38% of those over 60. This skepticism suggests that the younger generation is beginning to question the very financial wisdom of a system that demands so much for so little security.

Structural Implications and Future Outlook

The implications of this housing crisis extend far beyond the individual’s inability to own property. When young adults cannot build equity, they are unable to participate in the most significant wealth-building mechanism in American history. This creates a feedback loop of inequality: those who already own homes see their net worth grow through appreciation, while those who rent see their income eroded by rising rents, leaving them with less to save for future purchases.

Potential Policy Interventions

Economists and policy experts point to several areas for potential relief, though none are simple. These include:

- Supply-Side Reform: Addressing the chronic shortage of housing inventory through zoning reform and incentives for multi-family development.

- First-Time Homebuyer Support: Expanding federal and state programs that assist with down payments to mitigate the initial barrier to entry.

- Wage Alignment: Addressing the stagnation of real wages, particularly for entry-level professional roles, to ensure that income growth can eventually move in tandem with asset appreciation.

Conclusion: A Turning Point

The current housing market represents a significant pivot point in American social and economic life. As the gap between home prices and income widens, the country faces the prospect of a permanent "renter class," with profound consequences for social mobility and long-term economic health.

The data provided by the Pew Research Center serves as an urgent call for policymakers, urban planners, and the financial sector to re-evaluate the infrastructure of homeownership. Without meaningful intervention, the "American Dream" may soon be relegated to the history books, remembered as a feature of the 20th century that simply could not survive the economic realities of the 2020s.

For now, young adults are left navigating an environment where the cost of entry is at an all-time high, and the promise of stability remains, for most, just out of reach.