For nearly a decade, the Amazon marketplace functioned under a "growth at all costs" mandate. During this era, rising Cost-Per-Click (CPC) figures were viewed as a manageable friction point—a toll paid for the privilege of rapid scaling. If a brand saw ad costs rise, the solution was simple: expand the category, increase organic velocity, and let the sheer momentum of the platform hide the inefficiencies.

That era has officially ended.

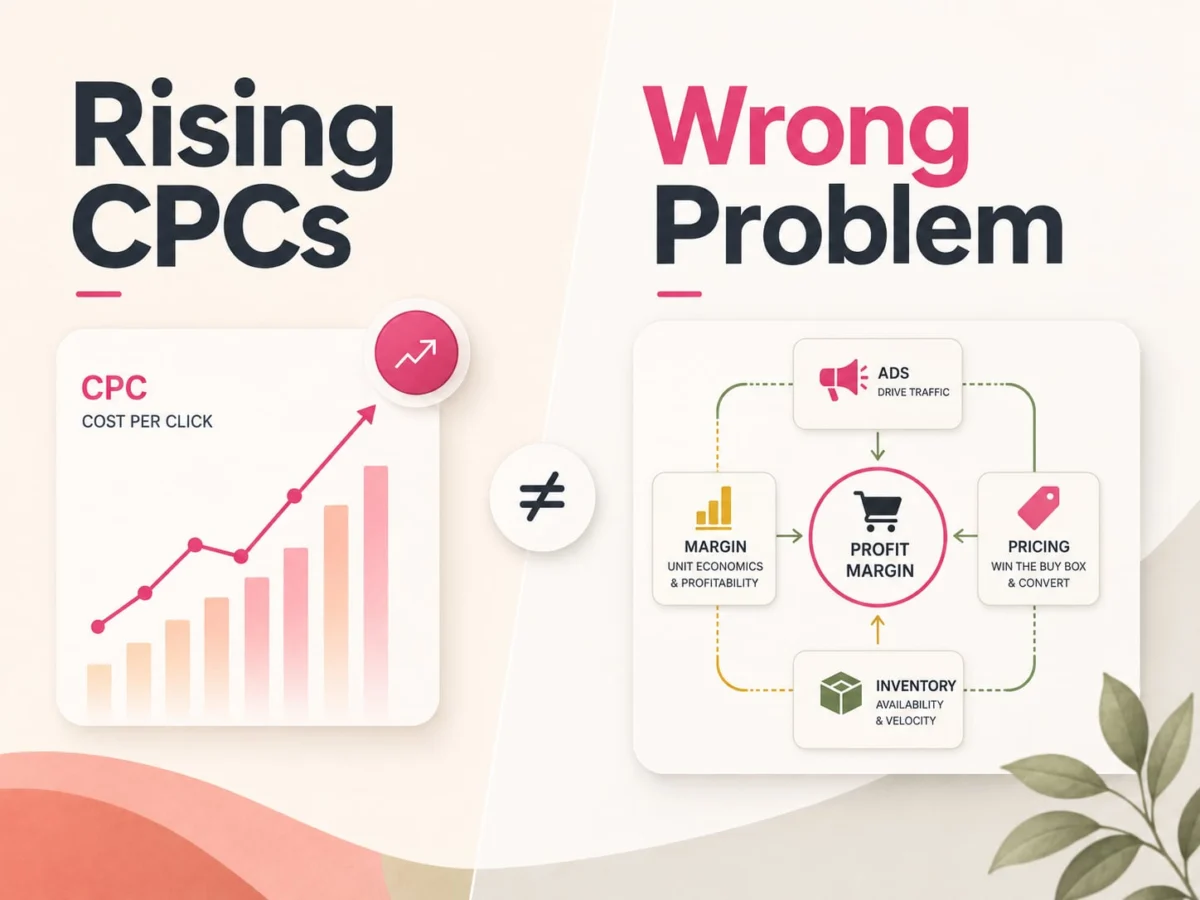

Recent data from the Trellis platform reveals a sobering trend: average CPCs have climbed approximately 10% year-over-year, while total ad spend has surged by 27%. This divergence indicates that brands are not just paying more for traffic; they are spending significantly more just to maintain their current market share, often experiencing diminishing returns in the process. We are no longer witnessing a mere increase in advertising costs. We are witnessing a fundamental shift where CPC inflation has matured into a structural threat to net profitability.

The Chronology of an Unfolding Crisis

To understand how we reached this inflection point, one must look at the evolution of the Amazon seller ecosystem.

Phase 1: The Land Grab (2015–2019)

In the early days, organic growth and "low-hanging fruit" keyword strategies allowed brands to survive with thin margins. CPCs were relatively stable, and ad spend was an optional lever rather than a requirement for survival.

Phase 2: The Sophistication Gap (2020–2022)

As the pandemic accelerated e-commerce, the "professionalization" of Amazon sellers began. The competitive edge shifted to those who mastered campaign mechanics—surgical keyword harvesting, automated bidding, and granular segmentation. During this time, automation was a distinct competitive advantage.

Phase 3: The Convergence (2023–Present)

Today, sophisticated automation is no longer a differentiator; it is the industry standard. Most established operators have access to the same tools and tactical playbooks. As campaign structures converge, the "edge" has evaporated. This has led to a market where competition is no longer defined by who has the best ad agency or the most aggressive bidding script, but by who has the most resilient financial architecture.

Supporting Data: The Compounding Pressure

The current threat to profitability is not a singular phenomenon; it is a convergence of multiple, compounding pressures that traditional ad metrics fail to capture.

According to platform data, the primary drivers of this structural change include:

- Ad Spend vs. Revenue Divergence: While total ad spend is up 27%, conversion rates in many categories have plateaued or dipped, forcing brands to bid more aggressively to maintain the same sales velocity.

- The "Visibility Tax": Because Amazon’s algorithm heavily weights sales velocity, brands are forced to maintain high ad spend to stay visible. If they throttle spend, ranking drops, which subsequently necessitates even higher future spending to regain lost ground.

- Operational Silos: The most significant data point is the disconnect between departments. Most brands still manage pricing, inventory, and advertising as three distinct silos, preventing the real-time adjustments required to combat CPC inflation.

The Blind Spot of Traditional Metrics

Many sellers remain tethered to metrics like ACoS (Advertising Cost of Sales) and ROAS (Return on Ad Spend). While these metrics are essential, they are inherently backward-looking and isolated. They provide a view of the "ad console" but ignore the broader Profit and Loss (P&L) reality.

A campaign may appear "efficient" in the ad console while simultaneously eroding the company’s net bottom line. For instance, a brand might achieve a target ACoS while ignoring that their inventory carrying costs or current promotional discounting have rendered that sale net-negative.

This creates a "blind spot" where sellers bid blindly against competitors who may have superior unit economics. In this environment, the strongest brands are not necessarily the ones with the lowest ACoS; they are the ones with the most robust contribution margins, allowing them to absorb higher CPCs without destabilizing their business.

The Strategic Imperative: Integrating Pricing and Advertising

The most profound realization for modern operators is that pricing is now an acquisition strategy.

When a brand treats pricing and advertising as separate decisions, they fall into a "Vicious Cycle of Coordination Failure." For example, a seller might raise prices to protect margins during a high-cost period. However, if the ad platform is not "aware" of this price change, it continues to bid as if the conversion rate remains constant. As the price increase inevitably softens conversion, the ad algorithm struggles, spend efficiency drops, and visibility suffers. To recover, the seller then resorts to deeper discounts—effectively wiping out the margin they sought to protect.

The Role of Dynamic Pricing

Dynamic pricing is no longer just a tool for capturing market share; it is a defensive mechanism against margin erosion. Implementing even minor, high-frequency price adjustments—such as two changes per week—can yield 2–5% in margin recovery.

When pricing and ad signals share a unified data layer, the ecosystem becomes responsive. If a price change is implemented, the ad algorithm can immediately adjust bids to compensate for the shifted conversion probability. This ensures that spend is concentrated where conversion is strongest, preventing the "hidden" erosion of profitability that occurs in manual environments.

Implications: The New Definition of Competitive Advantage

As we move deeper into this cycle of inflation, the definition of an "Amazon expert" is changing. The days of winning through sheer campaign mechanics are behind us.

1. Financial Resilience as a Weapon

In the current marketplace, you are not just competing against a brand’s bid; you are competing against their balance sheet. Brands with tighter inventory coordination and healthier margins can sustain aggressive acquisition cycles longer than their competitors. This "staying power" allows them to outlast rivals during periods of high CPCs or seasonal volatility.

2. Operational Integration

The winners of the next three to five years will be the companies that dismantle their internal silos. Marketing, finance, and operations must act in concert. An ad strategy that is not informed by real-time inventory levels and dynamic pricing is effectively operating with one hand tied behind its back.

3. Shift in Performance Philosophy

The goal is no longer to achieve the lowest possible cost for a click. The goal is to maximize the "sustainable acquisition limit." This is the highest CPC a brand can afford to pay while maintaining the profitability required to reinvest in future growth. Brands that understand their true contribution margin at the SKU level—and adjust their pricing and bidding accordingly—will inevitably capture market share from those who are merely chasing vanity metrics.

Conclusion: The Path Forward

The structural threat of CPC inflation is not going to subside. As more capital flows into the Amazon ecosystem and the marketplace matures, the "easy" gains are gone.

For brands looking to maintain their edge, the focus must shift from isolated optimization to comprehensive operational intelligence. By coordinating pricing, advertising, and inventory through a shared data framework, businesses can move from a reactive stance—where they are constantly fighting to maintain visibility—to a proactive stance, where they control the variables that dictate their success.

The brands that will stay profitable longest are those that understand that in a mature market, the most effective advertising strategy is not just about how you spend, but how you protect the margin that fuels that spending. In the battle for market share, your ability to absorb marketplace pressure is the ultimate competitive advantage.